WHAT’S THE WORST THAT COULD HAPPEN?

During periods of market volatility, financial advisors commonly tell clients to stay the course and fight any urge to de-risk. Long term charts of major equity averages show that even diversified portfolios experience significant drawdowns every once in a while, but have historically gone on to reach news highs every time. With conviction and a long enough time horizon, ignoring the price action can ultimately pay off.1

That approach doesn’t necessarily hold true for single stock exposures. Imagine owning pre-revenue dot-com companies in the very early 2000s, or financial stocks in 2007 as they began their declines (in some cases, to zero). Price often does lead fundamentals, and early declines can precede greater declines which later become clearly justified to all as expectations come down to earth or six feet under.

US cannabis investors currently face a lot of uncertainty, not least of which comes from the potential impact to profitability from a range of federal policy outcomes. Then there’s the issue of a broader equity bull market that feels long in the tooth after an unflinching 18-month, 100+% rally off the lows2. What could happen to high-beta assets at the edge of the risk spectrum if there is a broader flight to safety? Could ignoring the price action in cannabis operators ultimately pay off, or is there risk in holding as uncertainty resolves?

The recent experience of Plus Products Inc., a California-focused producer of cannabis-infused edibles, gives one answer. Just last month, the company reported record revenue and improving gross margins:3

This is music to the ears of investors who value securities using only the topmost portion of the income statement. The company also notes on its investor deck (dated August 2021) that it has “rock-solid fundamentals” with “sustainable cash burn”:4

But digging a little deeper, it’s clear that Plus has a history of unprofitability:5

In its Q2 MD&A, the company noted that “Management plans to continue its efforts to consider additional external financing through the issuance of equity and debt to finance the operations, expansion, and capital expenditures of the Company; however, there can be no certainty that such funds will be available on a timely basis and on terms acceptable to the Company” (emphasis added)6, while I wrote back in June that “When money is expensive […] management has a choice: run a lean operation or repeatedly tap the capital markets just to keep the lights on. The environment is a training ground that forces discipline and efficiency as a matter of survival.”

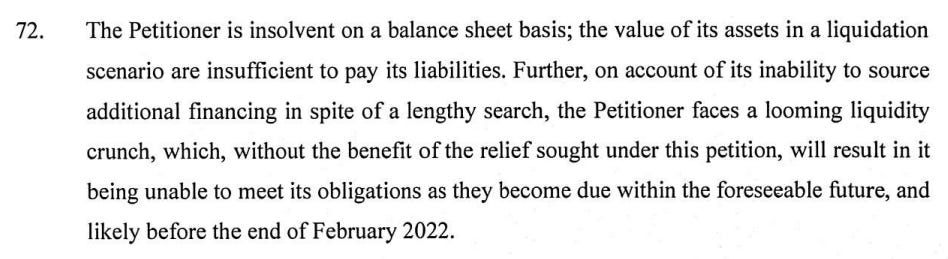

And as a matter of survival, Plus filed for protection from creditors in mid-September, just five weeks after the preparation of its Q2 financials, declaring itself unable “to source additional financing in spite of a lengthy search” and facing an inevitable liquidity crisis absent court intervention.7

Equity investors didn’t seem to anticipate this outcome. The stock mostly traded sideways from the COVID lows of March 2020, with some upside participation in the post-election enthusiasm that broadly benefited the sector. It clearly wasn’t hugging the zero bound in its final trading sessions before being halted and delisted at the company’s request8. So much for efficient markets.

With the stock now delisted, shareholders are effectively stuck in limbo. I don’t have a lot of insight into the Canadian process by which Plus has sought relief but intuitively, when courts force creditors to take losses the equity tends to become either worthless or effectively worthless via dilution. This experience shows there is risk to holding certain stocks through adverse financial conditions, and any investor who decided to “buy the ticket, take the ride” on a company that becomes subject to restructuring may wish that they hadn’t.

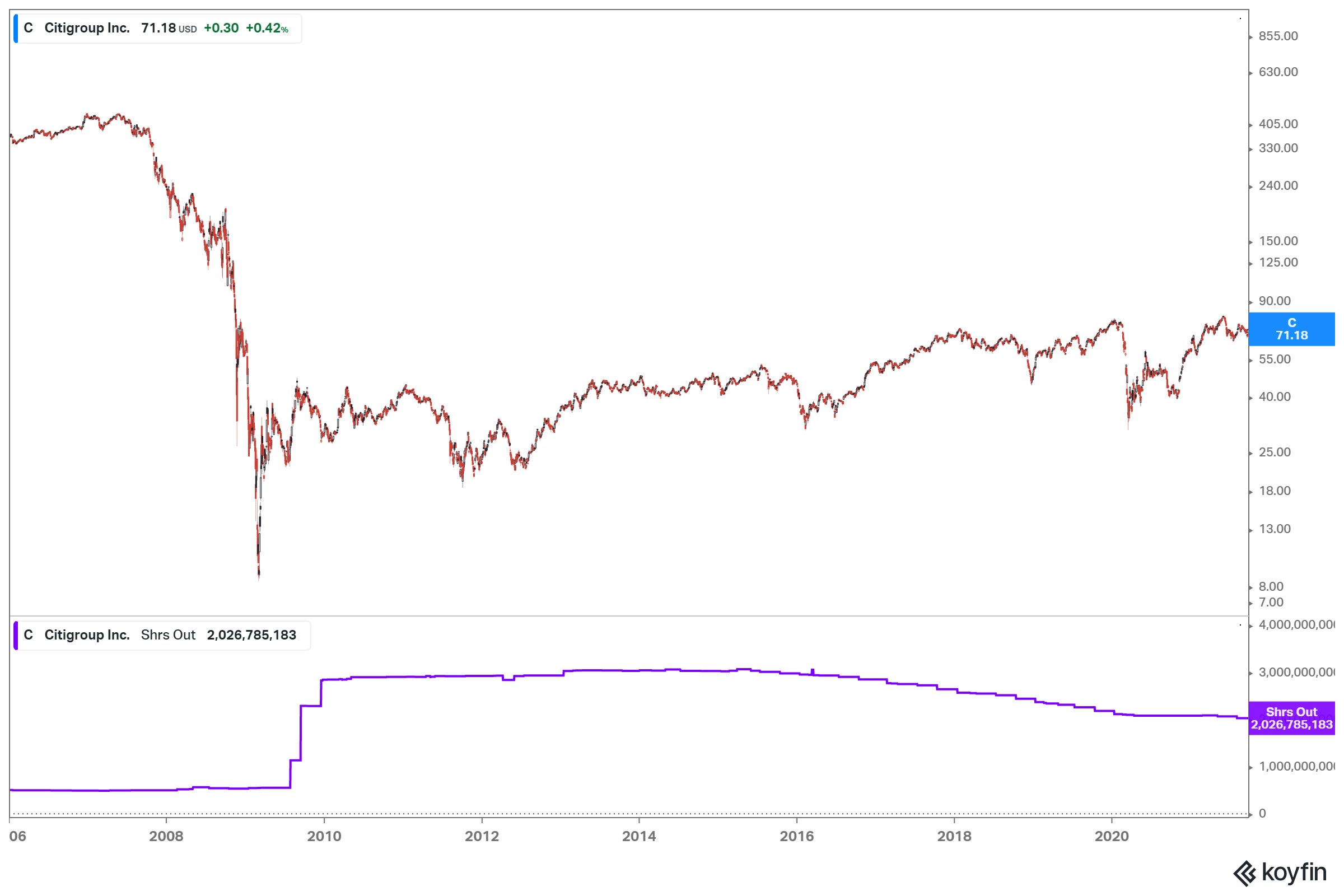

There is also a moderate downside scenario where courts aren’t involved but shareholders still suffer. Consider the experience of Citigroup and Goldman Sachs through the financial crisis. The two companies aren’t quite like-for-like but the impact of dilution on each set of shareholders is instructive (the lower graphs of the following charts show shares outstanding; note the y-axis of each):9

One of these firms had a toxic balance sheet going into the crisis while the other did not (or at least not after the federal government backstopped much of its risk). The difference in share performance is stark, with Citi still down over 80% nearly 16 years later:10

A weak balance sheet and reliance on external financing can be a formula for diminished shareholder returns even when courts aren’t involved.

With an increasing cost of equity capital11, a survival of the fittest environment is in full effect. We can see from Plus’ petition that there is a limit to the extent that lenders are willing to maintain or increase their exposure to unprofitable, cashflow-negative businesses. In contrast, firms that are able to fund operations and expansion with internal cash generation alone are likely at a material advantage.

Passage of the SAFE Banking Act could give a boost to profitable firms that are constrained by their existing debt load and service costs. However, banks might not want to load up their balance sheets with loans to borrowers that have a high probability of default. Lending standards may initially be high with preference given to operators that have a demonstrated consistency of profitability and can satisfy debt repayment via cash generation rather than via collateral liquidation upon default (as with any other sector).

One positive consequence of challenging financial conditions is that affected firms are less likely to engage in malinvestment and thus avoid creating a boom-and-bust cycle in the search for equilibrium in supply and demand. Creative destruction isn’t often allowed to run its course in a world of zero and negative interest rates but where it can, inefficient businesses are deprived of capital to fund operations. The rewards are then enjoyed by the customers and shareholders of companies that are able to deliver sustainable value via better products and higher profits.

So how to position on the winning side of the investment opportunity given the threats posed by a punishing environment, a broader risk-off move that could drag down high-beta assets, and the uncertain timing of federal policy reform? The issues I’m considering as I evaluate companies include:12

The state of the balance sheet including near-term liabilities

Cash generation and operating/pretax profit trends (not just gross profit), and the likelihood that each of these change for the worse (for example due to competitive pressures in each of the company’s operating markets)

EBITDA generation and availability of unencumbered collateral (an absence of which could impair access to funding)

Relationships with institutional lenders and investors

How much the decision makers are invested in the firm and how that might compare to the present value of their potential future interests after a restructuring

Any basis between the company’s investor marketing claims and its regulatory disclosures

I’m buying the ticket and taking the ride. But I think it’s worth digging in to see where the ride could go.

Subscribe to avoid missing the next issue! And follow along on Twitter for timely commentary.

DISCLAIMER

This material has been produced and distributed for informational purposes only. Sources for the information herein are believed to be reliable, but the information is not guaranteed as to accuracy and does not purport to be complete, and no representation or warranty is made that it is accurate or complete. The author undertakes no obligation to provide any additional or supplemental information or any update to or correction of the information contained herein. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation to buy, sell, or otherwise transact in such securities. The author shall not be liable in any way for any losses, costs or claims arising from reliance on this material, which is not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any investment or other matter. Past performance is no guarantee of future results. Securities discussed in this material may or may not be held in portfolios owned or controlled by the author at any given time.

Past performance is no guarantee of future results

Source: Koyfin.com, based on SPY price performance as at 9/24/21

Source: https://www.globenewswire.com/en/news-release/2021/08/04/2275120/0/en/Plus-Products-Achieves-Record-Quarterly-Sales-Reports-Second-Quarter-2021-Financial-Results.html

Source: https://www.plusproductsinc.com/static-files/926ae5e0-f14a-4fd7-89fb-f2f6eac49894 as at 9/28/21

Source: Q2’21 MD&A available on sedar.com

Source: Q2’21 MD&A available on sedar.com

Source: Plus’ petition to the court (including paragraphs 47, 51, 52 and 72); available from https://www.pwc.com/ca/en/car/plus-products/assets/plus-products-002_091421.PDF

Source: Koyfin.com

Source: Koyfin.com

Source: Koyfin.com

The US cannabis ETF MSOS has a price return of -12% year to date while many operators’ revenue and profitability metrics per share have increased over this period; source for MSOS price return: Koyfin.com as at 9/28/21

Plus notes in its petition that the stay was requested to enable a combined restructuring and sale of the business. To the extent that the firm’s decision makers remain at the new firm, the value of their diluted or written off economic interests could be subject to replacement post-restructuring. See paragraph 36 of Plus’ petition to the court, available from https://www.pwc.com/ca/en/car/plus-products/assets/plus-products-002_091421.PDF